0.5% Income Tax on All Merchants, Monitoring via Marketplace Data

JAKARTA, DDTCNews - The government has established a regulation imposing Art. 22 Income Tax of 0.5% on income derived by merchants trading on marketplace platforms. This issue has sparked widespread discussion among netizens over the past week.

Hestu Yoga Saksama, Director of Tax Regulations I of the Directorate General of Taxes (DGT), stated that the 0.5% income tax rate applies flat to both large and small-scale online merchants. Pursuant to MoF Reg. 37/2025, income tax will be collected and remitted by marketplaces designated as collection agents.

“Through MoF Reg. 37/2025, we mandate marketplaces to collect and remit the tax. We set the remittance at the final rate of 0.5%. This also applies to [large] merchants, as marketplaces don’t have access to all individual transactions. We, therefore, apply a flat rate,” he remarked.

Yoga explained that the income tax collection scheme for domestic marketplaces is stipulated under MoF Reg. 37/2025. Art. 22 Income Tax is imposed at a rate of 0.5% of the gross turnover received or accrued by online merchants.

Further, trade data submitted by marketplace providers to the DGT will serve as the basis for monitoring.

Yon Arsal, Assistant to the Minister for Tax Compliance Affairs, noted that revenues generated from Art. 22 Income Tax collection on marketplace transactions are not significant. However, data obtained from marketplaces may be used to support monitoring activities.

“The data will later be consolidated within the DGT system. This is what we will monitor and use to provide education to taxpayers,” Yon explained.

He illustrated that if the aggregated data indicates that a marketplace business owner has surpassed IDR4.8 billion in turnover, the business owner will be encouraged to report their business to be registered as a taxable person (pengusaha kena pajak/PKP in Indonesian).

Referring to Art. 15 paragraph (1) of MoF Reg. 37/2025, marketplace providers are required to submit a minimum of four types of information in respect of the trade of goods and services on marketplaces to the DGT.

First, the merchant’s taxpayer identification number (TIN or nomor pokok wajib pajak/NPWP in Indonesian) or national identification number (nomor induk kependudukan/NIK in Indonesian) and correspondence address, a statement from the domestic merchant stating that their turnover has or has not exceeded IDR500 million and an exemption certificate (surat keterangan bebas/SKB in Indonesian) submitted by the domestic merchant.

Second, other information, including the name, account name and/or country of choice of the domestic merchant; the TIN or tax identification number and/or correspondence address of the marketplace provider acting as the other party; and the email address and telephone number of the buyer of goods/services.

Third, information contained in documents equivalent to the Art. 22 Income Tax collection receipt. This information includes the number and date of the invoice; the name of the other party; the name of the domestic merchant account; the identity of the buyer of goods/services in the form of the name and address; the type of goods/services, total selling price and discount; and the amount of Art. 22 Income Tax for each domestic merchant.

Fourth, Art. 22 Income Tax collected and remitted by the marketplace provider.

On another note, MoF Reg. 37/2025 also requires marketplace providers to collect Art. 22 Income Tax at a rate of 0.5% of the gross turnover received by merchants as listed in the invoice documents.

Beyond this, several other noteworthy topics merit attention. These include the government’s online learning platform for participants of the tax consultant certification exam (ujian sertifikasi konsultan pajak/USKP in Indonesian), the release of the taxpayers’ charter and the DGT’s call for taxpayers to promptly perform overbooking.

The following is a comprehensive review of the tax articles.

Brace Yourselves, Online Merchants on Shopee and Tokopedia

The DGT is set to appoint marketplace operators, such as Shopee, Tokopedia and Bukalapak as Art. 22 Income Tax collection agents for the income of online merchants trading on these marketplaces.

Hestu Yoga Saksama stated that Art. 22 Income Tax levy applies to all online merchants, both large and small, operating via marketplace platforms. The applicable income tax rate amounts to 0.5%, as outlined in MoF Reg. 37/2025.

“Essentially, this regulation applies to all merchants on these marketplaces [Shopee, Tokopedia, Bukalapak and so forth],” he elaborated.

Marketplace Art. 22 Income Tax Is Creditable

The government is set to designate marketplace operators as collection agents of Art. 22 Income Tax of 0.5% on income received by all domestic online merchants–small, medium or large-scale.

Hestu Yoga Saksama stated that merchants whose annual turnover exceeds IDR4.8 billion are allowed to credit Art. 22 Income Tax collected by marketplace providers.

“For non-MSME large-scale businesses, the 0.5% Income Tax collected by the marketplaces will constitute a tax credit. The income tax is neither forfeited nor final,” he claimed.

USKP Participants Can Learn Online

Prospective participants of the 2025 tax consultant certification exam (ujian sertifikasi konsultan pajak/USKP in Indonesian) for periods II and III can now access a learning platform provided by the Ministry of Finance's Center for Functional Position Development and Quality Assurance (Pusat Pembinaan Jabatan Fungsional dan Penjaminan Mutu in Indonesian).

The open access (OA) e-learning platform offers taxation materials relevant to tax consultant certification exam levels A and B. These materials will be publicly accessible from 15-23 July 2025 on the official website of the Tax Consultant Certification Organizing Committee (Komite Pelaksana Panitia Penyelenggara Sertifikasi Konsultan Pajak/KP3SKP in Indonesian).

“Prospective USKP registrants can participate in the OA program free of charge,” said Nana Riana, Head of the Center for Functional Position Development and Quality Assurance at the Ministry of Finance.

DJP to Issue a Taxpayers’ Charter

The DGT is set to release the taxpayers’ charter next week.

The director general of taxes Bimo Wijayanto explained that the taxpayers’ charter is designed to provide certainty in terms of taxpayers’ tax rights and obligations.

“This initiative aims to provide legal certainty in the implementation of existing tax laws,” he said in a meeting with Commission XI of the House of Representatives (Dewan Perwakilan Rakyat/DPR in Indonesian).

Taxpayers Urged to Immediately Perform Overbooking Amidst Rising Deposits

The DGT is calling on all taxpayers to immediately file their tax payments via deposit in their tax returns (surat pemberitahuan/SPT in Indonesian).

The DGT stresses that tax payments via deposit do not waive the obligation to file tax returns. Failure of a taxpayer that has paid their tax via deposit to file tax returns may result in penalties, ranging from fines to reprimands.

“Taxpayers may still be subject to administrative penalties in the form of fines for delayed filing, the issuance of reprimand letters and other administrative measures as part of efforts to monitor tax compliance,” the DGT stated in its announcement. (sap)

Cek berita dan artikel yang lain di Google News.

KOMENTAR

ARTIKEL TERKAIT

Tak Dipungut PPh 22, Invois Marketplace Dianggap sebagai Bukti Pungut

Marketplace Luar Negeri Ikut Ditunjuk Jadi Pemungut PPh, Ini Alasannya

Jadi Pemungut Pajak, Marketplace Harus Setor Informasi Ini ke DJP

Tak Cuma Pedagang, Jasa Logistik di Marketplace Juga Kena PPh Pasal 22

berita pilihan

Mahasiswi STHI Jentera Terima Beasiswa Skripsi Sinergi Riset DDTC

Jual Beli Tanah, Begini Format Penulisan Alamat dalam Faktur Pajak

Jasa Ekspedisi Kena Tarif PPh 21 atau PPh 23? Ini Kata Kring Pajak

Catat! Jasa Asuransi Juga Bisa Dipungut PPh Pasal 22 oleh Marketplace

Mendagri Tito Dorong Pemda Bikin Satgas Percepatan Program MBG

Tarif Terbaru AS Bisa Jadi Angin Segar bagi Tekstil RI, Ini Kata API

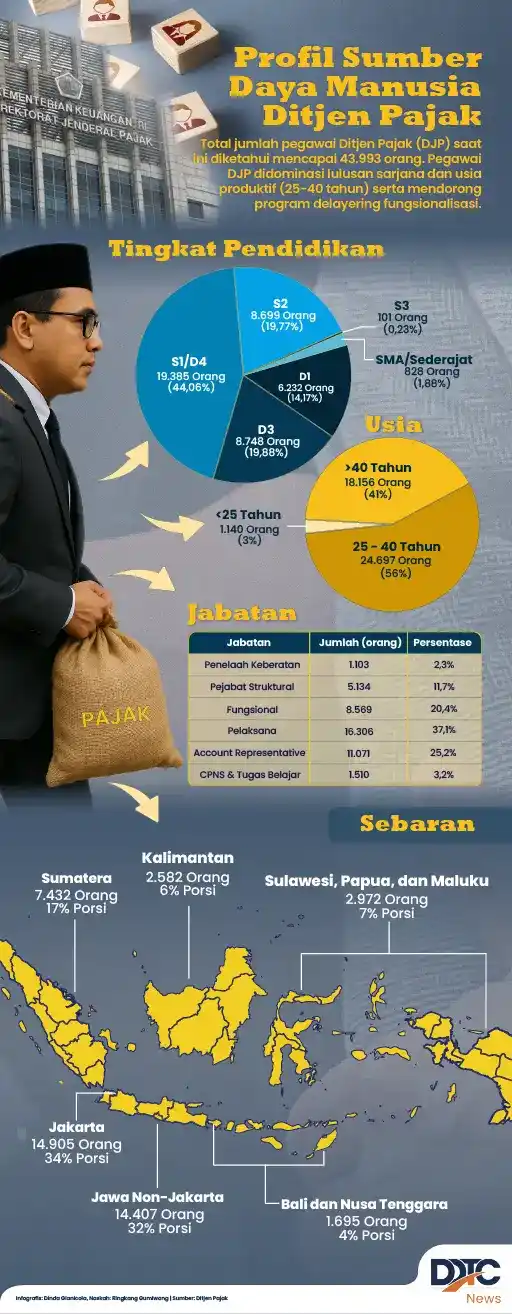

Sumber Daya Manusia di Ditjen Pajak dan Sebarannya

Kejari Bantu Cairkan Tunggakan Pajak, Nilainya Tembus Rp905 Juta

Koperasi Desa Merah Putih Bakal Dilengkapi Klinik dan Apotek Desa